Healthcare in Early Retirement: Options for Cleveland Pre-Retirees

A Westlake executive recently told us she wanted to retire at 60. She had the savings, the plan, and the timeline all worked out. What stopped her cold was one question: what happens to her health insurance for the five years before Medicare kicks in?

She is not alone. Healthcare is one of the biggest obstacles standing between pre-retirees and the early retirement they have worked toward. A healthy couple in their early 60s can expect to pay $1,500 to $2,000 a month or more for private coverage, and that number climbs every year. For many Cleveland-area professionals, the fear of that gap is enough to push retirement back by years it doesn't need to be.

The good news is that real options exist to bridge the gap to age 65. Here is what you need to know.

Why This Gap Matters

Medicare does not begin until age 65. If you retire earlier, even by a year or two, you need a coverage plan for that stretch. For a couple retiring at 60, that is five years of premiums, potentially $100,000 or more in total healthcare costs before Medicare even starts.

This is not a detail to figure out later. It needs to be part of your retirement date decision from the beginning, because the cost and availability of coverage can meaningfully shift your timeline or savings target.

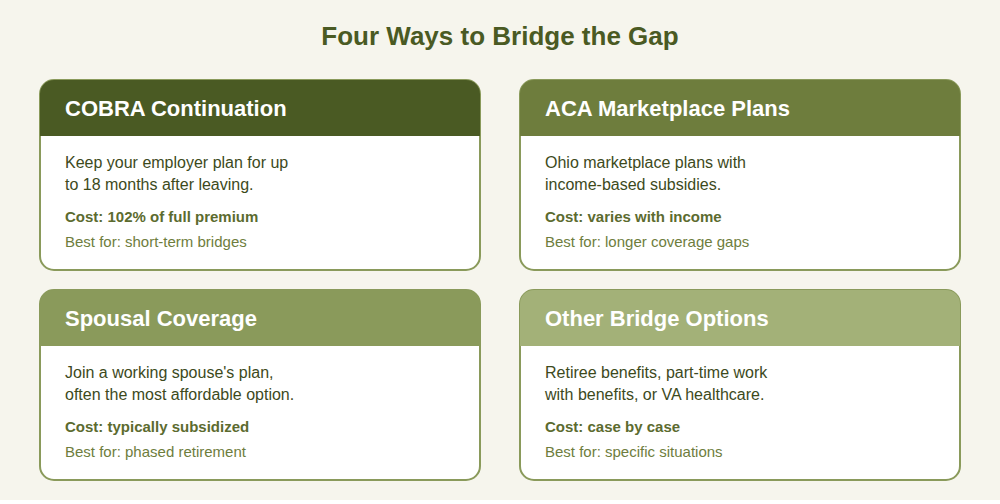

COBRA Continuation Coverage

COBRA lets you keep your employer's health plan for up to 18 months after you leave your job. You get the same coverage, the same network, and no medical underwriting, which makes it an easy transition.

The tradeoff is cost. You pay 102% of the full premium, since your employer is no longer subsidizing any of it. For many Cleveland-area professionals, that means $1,800 to $2,200 a month for family coverage.

COBRA tends to make the most sense as a short-term bridge, particularly if you are within 18 months of turning 65 or if you have ongoing medical needs that make network continuity valuable. Beyond that window, it is worth comparing against marketplace plans.

ACA Marketplace Plans

The Ohio health insurance marketplace, through Healthcare.gov, is often the more affordable long-term option for early retirees. Plans are organized into Bronze, Silver, Gold, and Platinum tiers, with Bronze offering lower premiums and higher out-of-pocket costs, and Platinum the reverse.

The real opportunity here is premium tax credits. These subsidies are based on your modified adjusted gross income relative to the federal poverty level, and they can dramatically reduce your monthly premium. A Cleveland couple managing their income carefully in early retirement, perhaps delaying large IRA withdrawals or strategically timing Roth conversions, can often qualify for substantial assistance.

This is where good planning pays off. Because subsidies are tied to taxable income rather than total assets, a couple with significant savings can still qualify for meaningful help if they manage withdrawals and capital gains thoughtfully in the years before Medicare. Silver plans also come with cost-sharing reductions for those who qualify, which further lower deductibles and out-of-pocket maximums.

Before choosing a plan, check that your Cleveland Clinic or University Hospitals providers are in network. Not all marketplace plans include the same provider networks, and this matters if you have established relationships with specific physicians.

Spousal Coverage

If one spouse is still working when the other retires, adding the retiring spouse to the working spouse's employer plan is often the simplest and most affordable option. It is worth comparing this cost to COBRA or a marketplace plan, since employer-sponsored coverage is often subsidized and may be less expensive even with an additional dependent.

This option also opens the door to a phased retirement approach, in which one spouse retires earlier while the other continues working to maintain coverage for both, then retires once the first spouse reaches 65.

Other Coverage Options

A few additional paths exist, though they fit fewer situations. Some employers, including a handful of larger Cleveland-area organizations, still offer retiree health benefits, though this is increasingly rare and worth confirming directly with HR. Health-sharing ministries are sometimes mentioned as an alternative, but they are not insurance and carry real limitations and risks that should be understood clearly before relying on them. Short-term health insurance plans offer very limited coverage and are generally not recommended beyond brief, temporary gaps. Part-time work that includes benefits is another option some retirees use to maintain coverage while easing into retirement. And if you have military service, VA healthcare eligibility is worth exploring as a coordinating piece of your overall coverage strategy.

Planning Strategies That Make a Difference

A Health Savings Account, if you have access to one while still working, offers a genuine triple tax advantage: contributions are deductible, growth is tax-free, and withdrawals for qualified medical expenses are never taxed. Building HSA savings before retirement gives you a dedicated, tax-efficient source of funds for healthcare costs during the bridge years.

Timing matters too. Retiring after 63 rather than 60 shortens the gap and can improve your subsidy eligibility. Managing taxable income carefully, through the timing of Roth conversions, investment sales, and any pension or lump sum decisions, can meaningfully affect how much you pay for coverage each year. We worked with a Cleveland-area couple who coordinated these pieces together: timing one spouse's retirement, structuring withdrawals to stay within subsidy thresholds, and using HSA funds for out-of-pocket costs. Their projected five-year healthcare bill dropped substantially as a result.

It is also worth setting aside a healthcare emergency fund in your plan. Even with good coverage, unexpected costs happen, and having a buffer protects the rest of your retirement plan from disruption.

The Transition to Medicare

Medicare begins the month you turn 65, with enrollment windows that carry real penalties if missed. We will cover Medicare parts A, B, D, and supplemental coverage in detail next month, but the short version is that your COBRA or marketplace coverage ends as Medicare begins, and the transition needs to be planned in advance rather than handled at the last minute.

Why This Belongs in Your Retirement Plan

Healthcare costs in early retirement are not a side issue. They are a core part of the retirement date decision, the income strategy, and the tax planning that goes into a comprehensive plan. A fiduciary advisor can model these scenarios alongside your broader financial picture, helping you see how coverage costs, subsidy planning, and your retirement timeline fit together.

Healthcare should not be the reason your early retirement dream stays on hold. With the right planning, the gap to Medicare is bridgeable.

If you are considering an early retirement and want to clearly understand your healthcare options, schedule a complimentary early retirement review with our Cleveland-area team. We will walk through the numbers together.