When Should You Claim Social Security? A Guide for Cleveland Couples

Tom and Linda had been looking forward to retirement for years. After successful careers at the Cleveland Clinic and a downtown law firm, Tom turned 62 and immediately filed for Social Security. "Why wait?" he reasoned.

Six months later, during dinner with friends in Rocky River, they learned their friends had a different strategy. The higher earner was waiting until 70 to claim, while the other spouse claimed earlier. Tom and Linda went home wondering if they had made a costly mistake.

They had. By claiming at 62 without considering a coordinated strategy, Tom potentially left over $100,000 on the table. Even worse, when he passes away, Linda's survivor benefit will be permanently reduced.

The Social Security claiming decision is one of the most important financial choices you'll make in retirement, and it's essentially permanent. For married couples, the complexity doubles. This guide will help you understand the key factors, strategies, and mistakes to avoid.

Social Security Claiming Basics: Understanding Your Options

You can claim Social Security retirement benefits anytime between the ages of 62 and 70. When you claim dramatically affects how much you receive each month for the rest of your life.

Your Full Retirement Age (FRA) depends on your birth year. For most people planning retirement today, it's between 66 and 67. At your FRA, you receive 100% of your calculated benefit based on your highest 35 years of earnings.

The Cost of Claiming Early: Claim at 62 when your FRA is 67, and you'll receive only 70% of your full benefit. That's a 30% permanent reduction. If your full benefit would be $2,500 per month, claiming at 62 means you'll receive only $1,750 instead. Over 20 years, that's a difference of $180,000.

The Reward for Delaying: For every year you delay past FRA (up to age 70), your benefit increases by 8% per year. Using the same $2,500 example, waiting until 70 means you'll receive $3,100 per month. That's an extra $600 every month for life, guaranteed and inflation-adjusted.

Key Factors in Your Claiming Decision

Health and Longevity Expectations

The break-even analysis is straightforward. If you claim at 62 versus 67, it takes until around age 78-83 to break even. Live past that point and delaying pays off.

But here's what many couples miss: it's not just about each individual. There's a 50% chance that at least one member of a 65-year-old couple will live to age 92. Consider your family history and health status, especially for the higher earner.

Financial Need and Other Income Sources

Do you actually need the Social Security income right now? Many Westlake and Rocky River couples we work with have substantial retirement savings, pensions, or other income. If you can comfortably cover expenses without Social Security until 70, delaying can be a powerful wealth-building strategy.

Just be careful not to convince yourself you "need" the money when what you really want is to start collecting. That emotional pull has cost many retirees significant money.

The Survivor Benefit Consideration

When one spouse passes away, the surviving spouse receives the higher of the two benefits but loses the smaller benefit entirely.

Let's look at a Strongsville couple, John and Mary. John's benefit at FRA is $3,000, and Mary's is $1,500. If both claim at FRA and John passes away at 80, Mary continues receiving John's $3,000 but loses her own $1,500. Their combined $4,500 monthly income drops to $3,000.

Now imagine if John had waited until 70, increasing his benefit to $3,720. When he passes, Mary receives that higher amount. That extra $720 per month could make a significant difference for the next 10-15 years.

This is why the higher earner should seriously consider delaying, even if it means tapping retirement savings in the meantime.

Tax Considerations

Social Security benefits can be taxable depending on your "provisional income." For couples with pensions, retirement account withdrawals, and investment income, a significant portion may be taxed. This creates planning opportunities by coordinating claiming with other income sources and possibly doing Roth conversions before you claim.

Claiming Strategies for Married Couples

Your claiming decisions affect each other, both while you're alive and after one of you passes away. The optimal strategy for married couples often involves different claiming ages for each spouse.

The "Higher Earner Delays" Strategy

This is one of the most powerful strategies, built on the survivor benefit principle. The higher earner delays claiming until 70 to lock in the maximum benefit. Meanwhile, the lower earner might claim earlier, depending on cash flow needs.

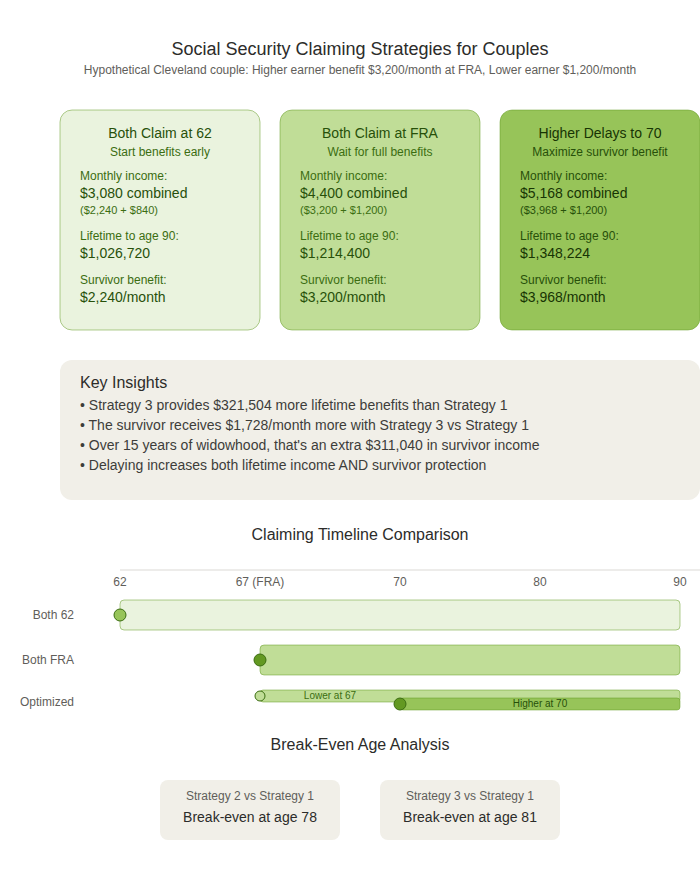

Let's look at a hypothetical Cleveland couple, Robert and Susan. Robert's benefit at FRA (67) is $3,200 per month, and Susan's is $1,200.

If Robert waits until 70, his benefit grows to $3,968. If Susan claims at 67, she receives her full $1,200. Together, they're receiving $5,168 monthly once Robert claims.

Here's the key: when Robert passes away, Susan receives his $3,968 as a survivor benefit. If Robert had claimed at 62 instead (reducing his benefit to $2,240), that's what Susan would be stuck with. By delaying, Robert bought Susan an extra $1,728 per month. Over 15-20 years of widowhood, that's potentially $350,000 or more.

Understanding Spousal Benefits

If you're married and your own benefit is less than half of your spouse's FRA benefit, you may be eligible for a spousal benefit instead. However, your spouse must have already filed for their own benefit.

The maximum spousal benefit is 50% of the higher earner's FRA benefit. If you claim before your own FRA, it will be reduced. There are no delayed retirement credits for spousal benefits, so there's no advantage to waiting past your FRA.

Social Security automatically pays you the higher amount between your own benefit and the spousal benefit.

The Split Strategy

Some couples benefit from one spouse claiming early and the other delaying. This works especially well when you need some Social Security income now but not both benefits, the higher earner is in good health, and the lower earner's benefit is modest.

For example, a Bay Village couple where one spouse's benefit at FRA is $2,800 and the other's is $1,400. If they need about $1,400 monthly from Social Security now, the lower earner could claim at 67 while the higher earner waits until 70.

Special Situations and Considerations

Government Pension Offset and Windfall Elimination Provision: If you receive a pension from work where you didn't pay Social Security taxes (common for some government employees and teachers in Ohio), two provisions may affect your benefits. WEP can reduce your own Social Security benefit, and GPO can reduce spousal or survivor benefits. If you have a pension from non-covered employment, you need specialized analysis.

Medicare Enrollment: Even if you're delaying Social Security, you generally must enroll in Medicare at 65 to avoid permanent late enrollment penalties, unless you have qualifying employer coverage. Social Security and Medicare enrollment are separate decisions.

Common Claiming Mistakes to Avoid

Claiming Too Early Without Full Analysis: The biggest mistake is claiming at 62 without running the numbers for your specific situation. If you can afford to wait, delaying often provides substantially more money over your lifetime.

Not Coordinating Between Spouses: Treating your claiming decisions as two separate choices rather than a coordinated strategy leaves money on the table.

Ignoring Survivor Benefit Implications: The higher earner focusing only on their own break-even analysis without considering the long-term impact on the surviving spouse is a critical error. There's a good chance one of you will live into your 90s, and that survivor will be living on one Social Security check instead of two.

Believing You Must Claim When Filing for Medicare: You must enroll in Medicare at 65 (unless you have qualifying employer coverage), but you can delay Social Security until 70 if you choose.

Creating Your Social Security Claiming Strategy

Start by asking yourself these questions:

- What's our household cash flow need in retirement?

- Can we comfortably delay one or both Social Security benefits?

- What's our health status and family longevity history?

- What other income sources do we have?

- How much do we value maximizing the survivor benefit?

The best way to make an informed decision is to model multiple scenarios: both spouses claiming at 62, both at FRA, both at 70, and various combinations. Look at each scenario's impact on annual income, taxes, and lifetime benefits under different longevity assumptions.

Social Security isn't an isolated decision. It connects to your retirement account withdrawal strategy, tax planning, Medicare planning, and estate planning. A comprehensive financial plan integrates all these pieces to optimize your overall financial picture.

Making Your Decision with Confidence

Your Social Security claiming decision is one of the most consequential financial choices you'll make. For Cleveland-area couples, getting this right can mean hundreds of thousands of dollars in additional lifetime benefits.

There's no one-size-fits-all answer. The optimal strategy for a Westlake couple with a pension and substantial savings will look different from a Rocky River couple who needs Social Security income to cover expenses.

What matters most is that you understand how Social Security works, model multiple scenarios for your situation, consider survivor implications, and integrate your claiming strategy with your overall financial plan.

With proper analysis and planning, you can confidently navigate this decision and maximize your benefits.

Ready to create your personalized Social Security claiming strategy? Schedule a complimentary consultation with our Westlake team to analyze your specific situation and explore what strategy works best for you and your spouse.