Where Does Retirement Income Come From?

Sarah and Jim were five years from retirement when they sat down at their kitchen table in Bay Village, their financial statements spread across it. They had saved diligently, maxed out their 401(k)s, and felt pretty good about their nest egg. But as they stared at the numbers, a question hit them: "Okay, we have $1.2 million saved. But where will our actual monthly income come from?"

It's a question many Cleveland-area professionals ask as they approach retirement. You've spent decades accumulating assets, but the shift to generating a reliable income from them requires a completely different approach. Understanding your retirement income sources and how they work together is essential to maintaining your lifestyle throughout retirement.

The Traditional Three-Legged Stool Has Changed

Financial planners used to talk about retirement as a three-legged stool: pension, Social Security, and personal savings. For many Westlake and North Olmsted retirees, that stool looks very different today.

Most companies have shifted from traditional pensions to 401(k) plans, placing retirement planning squarely on your shoulders. Social Security remains important, but it was never designed to fund your entire retirement. The reality? Today's retirees need to actively create their own retirement paycheck by strategically coordinating multiple income sources.

The good news is that with proper planning, you have more control and flexibility than previous generations. Let's break down where your retirement income will actually come from.

Social Security Benefits: Your Foundation

For most retirees, Social Security provides a foundational source of income. In 2026, the average Social Security benefit is around $1,900 per month, though benefits vary widely based on your earnings history.

Social Security typically replaces about 30-40% of pre-retirement income for middle and upper-income earners. A Cleveland couple who both work might receive combined benefits of $4,000 to $5,000 per month. That's meaningful income, but it rarely covers everything.

Your benefits are calculated based on your highest 35 years of earnings. The maximum benefit in 2026 for someone claiming at Full Retirement Age is approximately $3,800 per month. Benefits include annual cost-of-living adjustments (COLAs) to help keep pace with inflation.

Timing matters significantly. As we discussed in our recent guide to Social Security claiming strategies, when you claim can affect your lifetime benefits by hundreds of thousands of dollars, especially for married couples considering survivor benefits.

One important consideration: depending on your other income, up to 85% of your Social Security benefits may be taxable at the federal level. This makes tax planning essential as you coordinate your various income sources.

Employer Retirement Plans: Your Primary Resource

For most Cleveland-area professionals, 401(k) or 403(b) accounts represent the largest source of retirement income.

401(k) and 403(b) Accounts: These tax-deferred accounts have grown throughout your career, and now it's time to start withdrawals. Every dollar you take out is taxed as ordinary income. Required Minimum Distributions (RMDs) begin at age 73 or 75 depending on birthyear, forcing you to withdraw a percentage each year, whether you need the money or not.

A Westlake executive with $750,000 in their 401(k) might withdraw $30,000-$35,000 annually (around 4-4.5%) to supplement other income sources. The key is to create a sustainable withdrawal rate that allows your portfolio to last throughout a 25-30-year retirement while adjusting for market conditions.

Traditional Pensions: If you're fortunate enough to have a pension from an employer like University Hospitals or a government position, this provides a guaranteed monthly income. You'll typically choose between a single life annuity (higher payment, ends at your death) or a joint and survivor option (lower payment, continues for your spouse). This decision is permanent, so careful analysis is crucial.

Rollover IRAs: Many retirees consolidate old 401(k)s into IRAs for simplified management and often lower fees. Withdrawals work the same way as 401(k)s, taxed as ordinary income with RMDs starting at 73 or 75.

The traditional guideline has been the "4% rule," withdrawing 4% of your portfolio in year one and adjusting for inflation thereafter. While this provides a starting point, your actual withdrawal rate should be flexible based on market performance, your spending needs, and other income sources.

Personal Investment Accounts: Tax Flexibility

Beyond retirement accounts, personal investment accounts provide valuable flexibility in retirement.

Taxable Brokerage Accounts: These accounts offer significant advantages. Investment gains receive preferential long-term capital gains tax treatment (0%, 15%, or 20%, depending on income), which is often lower than ordinary income rates. You can withdraw any amount at any time without penalties, making these accounts perfect for bridging the gap if you retire before 59½.

Roth IRAs: Roth accounts are the crown jewel of retirement income planning. Withdrawals are completely tax-free in retirement, and there are no RMDs during your lifetime. Many Cleveland physicians and executives we work with use Roth IRAs strategically to manage their tax bracket in retirement. For example, in a year when you need extra money for a large expense, Roth withdrawals won't push you into a higher tax bracket or make more of your Social Security taxable.

Real Estate and Other Investments: Some retirees supplement income through rental properties or Real Estate Investment Trusts (REITs). These can provide steady cash flow, though rental properties require active management or a property manager.

Other Income Sources to Consider

Beyond the primary sources, several other options might play a role in your retirement income plan:

Part-Time Work or Consulting: Many retirees in Avon and Westlake continue working part-time, not just for income but for purpose and engagement. Flexible consulting in your field of expertise can provide meaningful income while maintaining professional connections.

Annuities: While not right for everyone, certain annuities can provide guaranteed lifetime income. Fixed or deferred income annuities might make sense for a portion of your portfolio if you want additional guaranteed income beyond Social Security and pensions. However, annuities are complex and often come with high fees, so they require careful evaluation.

Health Savings Accounts (HSAs): If you've been contributing to an HSA, these funds can be withdrawn tax-free for qualified medical expenses in retirement, making them valuable for healthcare costs.

Deferred Compensation or Business Sale: Executives with deferred compensation plans or business owners selling their companies may have additional income streams to coordinate.

Creating Your Retirement Income Plan

Now that you understand the sources, how do you put them together?

Start by estimating your annual retirement expenses. Most retirees need 70-80% of their pre-retirement income, though this varies by lifestyle, debt levels, and plans for travel or hobbies.

Next, map your income sources to your expenses. Social Security might cover your basic living expenses. Your 401(k) withdrawals cover discretionary spending. Your Roth IRA serves as a tax-free emergency fund.

Tax-efficient withdrawal sequencing is critical. A common strategy is to:

- Use taxable accounts first (while in lower tax brackets)

- Delay Social Security and tax-deferred accounts when possible

- Tap Roth accounts strategically to manage tax brackets

- Consider Roth conversions in low-income years

Many financial advisors recommend a bucket strategy organized by time horizon:

- Years 1-3: Cash and short-term bonds (stability and access)

- Years 4-10: Balanced portfolio of bonds and stocks

- Years 11+: Growth-oriented investments to outpace inflation

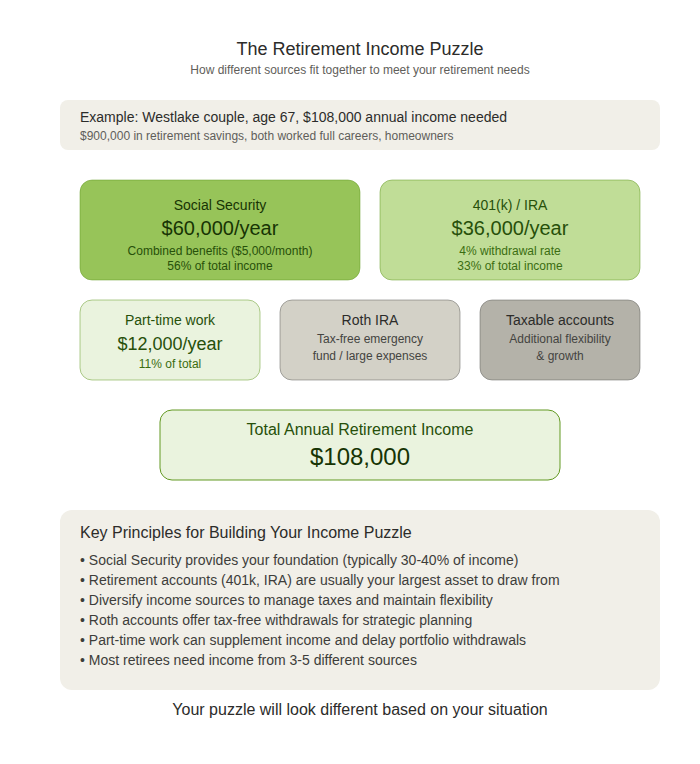

Let's look at a complete example. A Westlake couple retiring at 67 with $900,000 saved might structure their income like this:

- Social Security: $5,000/month combined ($60,000/year)

- 401(k) withdrawal: $36,000/year (4% of $900,000)

- Part-time consulting: $12,000/year

- Total income: $108,000/year

This provides a comfortable income while allowing flexibility. In years with strong market returns, they might withdraw less from the 401(k). If they need a new car, they tap the Roth IRA without tax consequences.

Working with a Fiduciary Advisor

Retirement income planning is complex. You're coordinating Social Security timing, tax-efficient withdrawals across multiple account types, investment management, RMD planning, and adjusting for life changes.

A fiduciary financial advisor helps you optimize these decisions based on your complete financial picture. We model different scenarios, coordinate tax strategies, and adjust your plan as markets and your needs evolve. Our goal is to help you confidently navigate the transition from accumulation to distribution, ensuring your money lasts throughout retirement while maintaining the lifestyle you've worked hard to achieve.

Your Retirement Income Roadmap

Most retirees will need income from multiple sources: Social Security, retirement accounts, personal investments, and possibly part-time work or other sources. The key is creating a coordinated plan that maximizes tax efficiency, provides the income you need, and maintains flexibility for life's unexpected turns.

Start planning five to ten years before retirement. The earlier you understand where your income will come from and how the pieces fit together, the more confident you'll feel as you approach this major life transition.

Ready to create your retirement income plan? Schedule a complimentary retirement income review with our Westlake team. We'll help you understand your income sources, optimize your withdrawal strategy, and build a plan that provides confidence throughout retirement.